The Consumer Financial Protection Bureau advanced its overhaul of annoying, incomprehensible mortgage forms on Wednesday in its first regulatory maneuver since the agency was created by last year's financial reform bill.

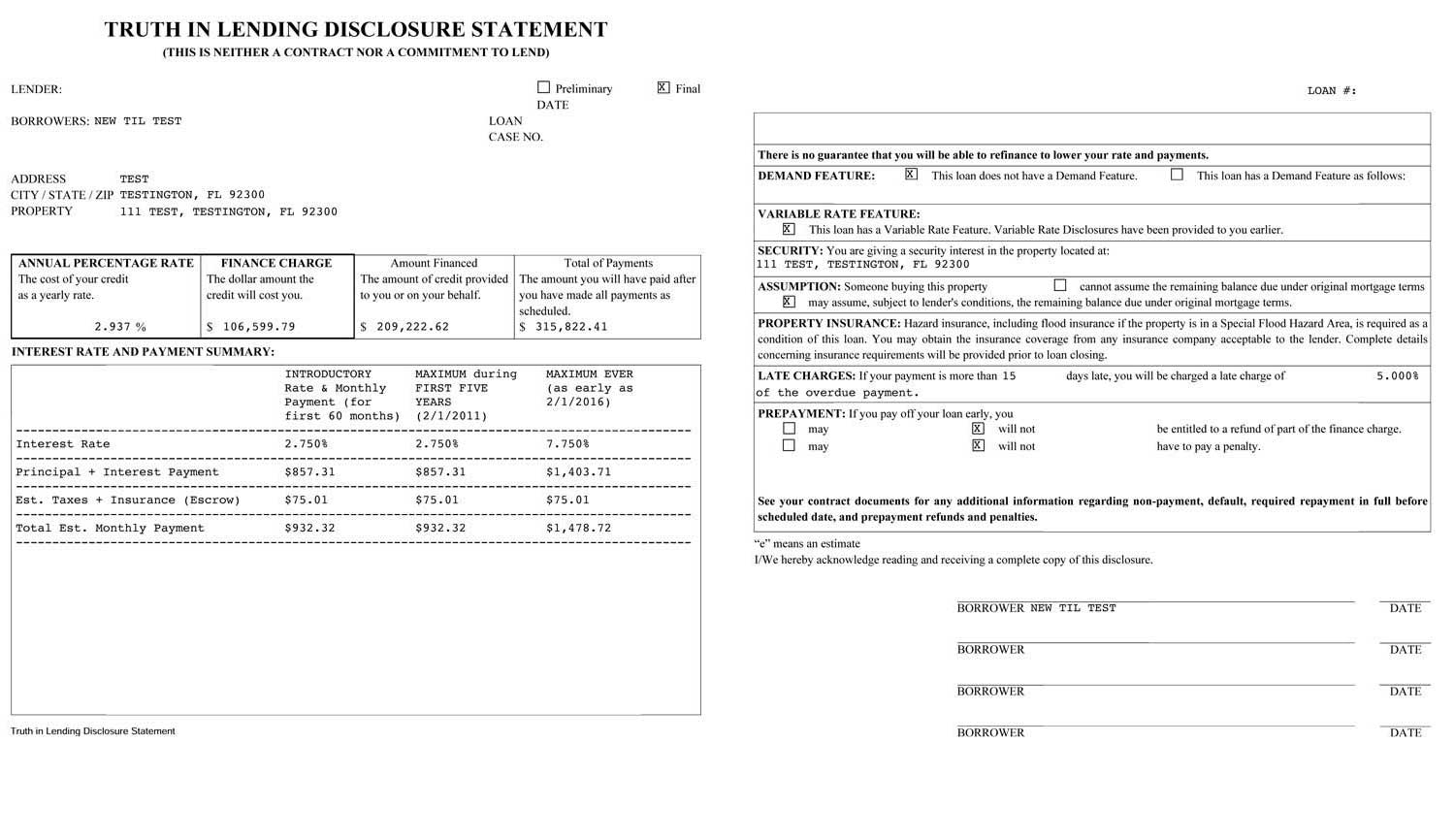

The CFPB rolled out two prototypes for a single, streamlined form to replace two complex and overlapping forms used by consumers to help gauge the real costs of their mortgage. The new regulator, which hopes to have a final form ready by September, is asking consumers to provide feedback on the forms online and is conducting in-person tests and interviews about the forms in six cities.

Consumer advocates and both community and Wall Street banks have lobbied for the change for years. Banks complain that it makes no sense for them to have to deal with two forms that carry the same basic information, while consumer advocates bemoan the fact that the forms aren't actually very helpful to consumers.

"The new forms -- they look good," said Ron Haynie, President and CEO of the Independent Community Bankers Association's mortgage group, which lobbies on behalf of small, community banks.

"This moves in a direction that makes sense," said Bob Davis, Executive Vice President of Mortgage Finance for the American Bankers Association, which represents banks of all sizes but traditionally places a heavy emphasis on the interests of big banks. "Our bankers thought this was a positive step."

Ira Rheingold, Executive Director of the National Association of Consumer Advocates also praised the new forms. "They've really got the right idea."

"You want consumers to actually be able to shop around for a mortgage," Rheingold said. "This information has to give consumers a legitimate view of the costs of the mortgage -- and that doesn't really exist today. The [current] forms are fairly incomprehensible, there's all sorts of numbers in there, and you can't tell what's important and what's not."

Once the new form is finalized, bankers may eventually begin butting heads with borrowers over its legal status. Currently the disclosure forms are not legally binding documents and banks could present the borrower with different final terms than the one outlined in the documents. But consumer advocates want the new forms to be a legally binding offer.

But for now, at least, both consumer advocates see this as a good sign of things to come.

Ed Mierzwinski, Director of the U.S. Public Interest Research Group's Consumer Program said CFPB's early testing process suggested the agency "has new ideas, not only about making disclosures better, but about making the regulatory process better for both buyers and sellers."

Elizabeth Eurgubian, Vice President and Regualtory Counsel for the ICBA added, "This process thus far has been a lot better for banks and for lenders than the previous processes have been, and the banks appreciate being brought in."

Take a look at the new prototypes here and here.

And compare them to the old forms here and here.

---------------

The CFPB rolled out two prototypes for a single, streamlined form to replace two complex and overlapping forms used by consumers to help gauge the real costs of their mortgage. The new regulator, which hopes to have a final form ready by September, is asking consumers to provide feedback on the forms online and is conducting in-person tests and interviews about the forms in six cities.

Consumer advocates and both community and Wall Street banks have lobbied for the change for years. Banks complain that it makes no sense for them to have to deal with two forms that carry the same basic information, while consumer advocates bemoan the fact that the forms aren't actually very helpful to consumers.

"The new forms -- they look good," said Ron Haynie, President and CEO of the Independent Community Bankers Association's mortgage group, which lobbies on behalf of small, community banks.

"This moves in a direction that makes sense," said Bob Davis, Executive Vice President of Mortgage Finance for the American Bankers Association, which represents banks of all sizes but traditionally places a heavy emphasis on the interests of big banks. "Our bankers thought this was a positive step."

Ira Rheingold, Executive Director of the National Association of Consumer Advocates also praised the new forms. "They've really got the right idea."

"You want consumers to actually be able to shop around for a mortgage," Rheingold said. "This information has to give consumers a legitimate view of the costs of the mortgage -- and that doesn't really exist today. The [current] forms are fairly incomprehensible, there's all sorts of numbers in there, and you can't tell what's important and what's not."

Once the new form is finalized, bankers may eventually begin butting heads with borrowers over its legal status. Currently the disclosure forms are not legally binding documents and banks could present the borrower with different final terms than the one outlined in the documents. But consumer advocates want the new forms to be a legally binding offer.

But for now, at least, both consumer advocates see this as a good sign of things to come.

Ed Mierzwinski, Director of the U.S. Public Interest Research Group's Consumer Program said CFPB's early testing process suggested the agency "has new ideas, not only about making disclosures better, but about making the regulatory process better for both buyers and sellers."

Elizabeth Eurgubian, Vice President and Regualtory Counsel for the ICBA added, "This process thus far has been a lot better for banks and for lenders than the previous processes have been, and the banks appreciate being brought in."

Take a look at the new prototypes here and here.

And compare them to the old forms here and here.

{kind=link}

---------------

The Truth About

Pepper Spray

No comments:

Post a Comment